Gulke: Stocks Surprise Again

The views expressed are those of the individual author and not necessarily those of DTN, its management or employees.

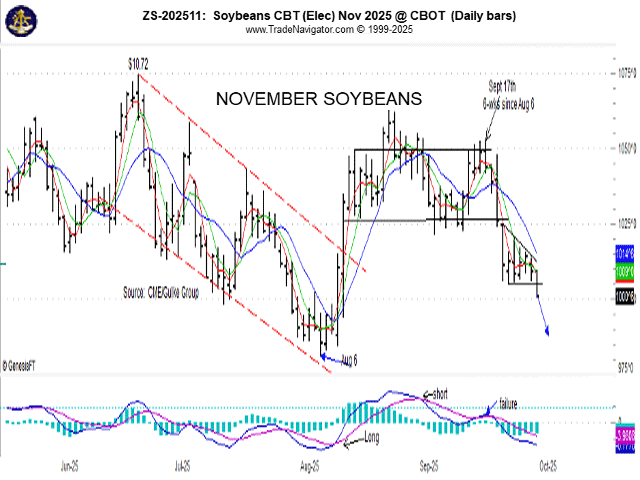

(Chart by Gulke Group)

As if the debate over supply and demand over the past 18 months hasn’t been contentious enough, we got another surprise on Tuesday from an ending stocks standpoint that makes data-driven reports all the more questionable and comes with terrible timing for some.

The overstatement of stocks over a year ago of what would be left on Aug. 30, 2025, went from 2.1 billion bushels (bb) to 1.325-plus bb to Tuesday’s final of 1.532 bb — a 207-million-bushel (mb) increase in carry-in to the 2025-26 marketing year. That increases carryout to 2.317 bb for the end of 2025-26 one year from now. One can argue the reasons for the increase. I have my opinion; they have theirs, and you have yours. But the undeniable bottom line is that confidence in data-driven guidance whipsaws markets to our detriment.

The debate over corn yield — whether it is 188 bushels per acre (bpa), 186 bpa or less — is a moot point, as USDA just found about 2 bpa more already in the bin. The September 2025 WASDE reflected a 2.11-bb carryout, so assuming the increase in incoming stocks goes directly to the bottom line, carryout increases to 2.317 bb and now needs to see a commensurate or bigger reduction in 2025 yields. If the government is funded by Oct. 10, we may see another shock. If not, we are left to the private sector for estimates.

In the meantime, our government has elected to kick the can down the road regarding the benefits of tariffs for ag, if any, opting to send checks again to tide us over. Both parties seem to agree that they can fix economic problems by sending subsidies. It seems like Econ 101 hasn’t changed, regardless of how the ecopolitical events are spun.

PRICE DISCOVERY

Disappearance of our production is a matter of demand, and price is determined by the amount of supply that will support demand. Too much demand versus supply says price discovery leads to a higher price, such that someone can’t afford to use it. Too much supply versus demand says price discovery determines a price to increase demand.

Our situation is one of global demand and global competition that is price-determined. Tariffs, non-tariffs, subsidies or buying up grains for food for peace — or whatever the nomenclature — doesn’t necessarily increase global demand. Put in simple terms, there is a global pie of demand and how it is sliced is determined by who will sell it the cheapest, not who is necessarily the lowest-cost producer. Argentina’s recent dumping of soybeans and soy oil to China and India is an example of we producers competing not with another farmer but with nations, a situation difficult to win.

If the situation of low prices isn’t enough, there is a dilemma for the producer who is caught having to sell off the combine or pay commercial storage. There are different schemes out there at various locations, and those vary with corporations, private companies or co-ops. Basis varies for soybeans, for example, from minus $1.50 or more in the Northern Plains to areas in the Corn/Bean Belt where it is rumored that a premium is paid for dry beans. Storing to Feb. 1, can vary in cost from 20 to 40 cents withing a 25-mile radius.

As most of you know, beans at 9% are 4% less than required, but we don’t get paid for dry matter. That is something I find unreasonable, but there has been no change for decades. Most years, beans start at 15%-16% and drop, making blending on-farm or at an elevator a profit center often worth 70 cents or more. This year, they are dropping to 8% during the day, making early morning combining a must for about three to four hours. Without wet beans, blending doesn’t work this year for the producer or the buyer.

USDA’s soybeans report on Tuesday was a non-event, but still, soybeans broke down again, signaling more to come, as harvest is open for the next 10 days or more without appreciable rain. That makes the decision to reduce income by $50 per acre and harvest dry or wait for rain and risk pods opening and money falling on the ground.

Personally, the soybean market looked promising from the EPA developments, but biodiesel demand using soy oil is now fraught with concerns that canola out of Canada and used cooking oil out of China may both be in play if we make nice with either country. India imports from Argentina, while our administration is pledging to help Argentine currency drain.

The November soybean price chart accompanying this week’s column shows the development that changed my mind about storing anything commercially and/or on farm without hedging off risk. Commercial storage at 40 cents to Feb. 1 won’t earn the cash bid and ends up being a negative ROI. If and when I see a strong enough buy signal to make me want to own soybeans, it will be on paper; it is cheaper, and I have flexibility to hold ’em or fold ’em.

November soybeans traded at $10.72 but couldn’t post highs over the 2025 high posted Feb. 21. The Aug. 6 low was met with a six-week typical bull market, which I spoke about in this column. It ended on Sept. 17 despite a seemingly friendly September WASDE, as if to spell before the fundamental fact that China was going to play us like a fiddle. Then, there was a pause the last six days that some media types reflected was a “pause that refreshes,” only to find a negative reaction to the stocks report on Tuesday.

Even to the casual observer, the direction is obvious unless some price miracle occurs shortly. Will China bail us out? Will we see a flash sale of someone just itching to buy what looks relatively cheap? Or will producers in a rush to finish harvesting decide to throw in the towel, as some buyers hope will happen? The stocks report showed 18% less on-farm stocks of beans, something we discussed since June 30 that “might” temper farmer selling. The cost to store, extra drying, etc., made my decision a little easier to sell off the combine any unsold/unhedged soybeans. Even the hedged soybeans are sold, letting the hedge ride a bit. A call to replace got cheaper on Tuesday and much cheaper than the cost to store commercially.

For the on-farm storage option, the media seems to make it easy. Store the soybeans — or corn, for that matter — as the market is paying more for July than now! That is half the story. The real question is will corn and/or soybeans be priced in July when July comes, or will it fade as the front month has. That’s a discussion for another time.

Jerry Gulke can be reached at (707) 365-0601 or by email at Jerry@gulkegroup.com

(c) Copyright 2025 DTN, LLC. All rights reserved.