Gulke: WASDE Unanswered Questions

The views expressed are those of the individual author and not necessarily those of DTN, its management or employees.

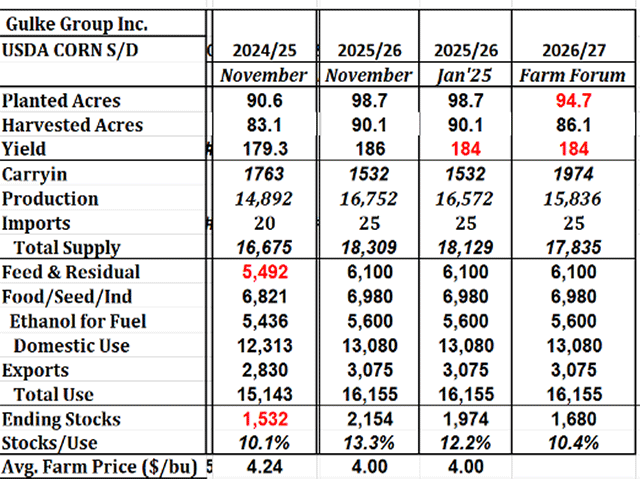

(Chart by Gulke Group)

Last week, market participants were looking ahead, trying to anticipate what WASDE would print after such a long time in a data-starved environment. All that is behind us now, with some current data coming in a timely manner and past data — whatever it’s worth — coming in a rather hodgepodge manner. But key items last Friday came as a surprise.

Surprise No. 1 was a minuscule drop in corn yield.

Surprise No. 2 was a drop in soybean exports, where one would have expected, at worst, an unchanged number, giving China more time to make a move.

Surprise No. 3 was that while WASDE reduced corn feed and residual use from 5.675 billion bushels (bb) to 5.492 billion bushels to account for that 200-million-plus-bushel increase in 2024-25 ending stocks to 1.532 bb from 1.302 bb.

You recall this writer questioned estimated ending stocks being 700 million bushels (mb) too high back in January 2024. It took WASDE nearly 18 months to reconcile, only to add back 200-plus mb in the Sept. 30 2024-25 final stocks number.

The unchanged yield in Surprise No. 1 was met with disbelief from most analysts. Lowering exports of soybeans made no sense, it seems, unless WASDE knows more about the final details of the U.S.-China agreement than participants themselves. But No. 3 is the real head scratcher.

Are we to assume feed usage will increase 600 mb this marketing year? Odds are that with an unchanged yield, the residual component is seen as the place to bury disappearance. Such a move brings more disbelief in reports. If the report had admitted feed and residual were too high last year and overstated proportionately for the coming 2025-26 we are in, the carryover would have been much higher, and price response would have been much worse. Questions remain!

Let’s assume USDA recognizes the error of its ways and reduces corn yield by 2 bushels per acre (bpa) to 184 bpa in its final report on Jan. 12, 2026, but leaves the 6.100 bb feed and residual unchanged. Carryout would drop to 1.974 bb but would be a plague on 2026-27 carry-in at a more than 400-mb increase over what we had to deal with this year. This would necessitate at least a 4-million-acre drop in corn planting, likely going to soybeans where they will be needed.

Media rhetoric is full of financial problems due to low corn prices and exploding input prices for almost everything except fuel. So, what if USDA decides to lower feed and residual use in its WASDE report 350 mb to 400 mb, where it probably should be? Carryout rises easily to over 2.1 bb again and doesn’t help the financial situation, plus makes the following year of 2027-28 just as challenging.

If USDA isn’t being proactive in looking ahead and seeing what their involvement could become, perhaps they should. At a minimum, producers should look ahead.

Currently, CZ26 is trading about 32 cents premium to CZ25, or about $60/acre better. The $4.68 price is a far cry from the low for CZ25 of $3.97 at the end of August, about $140/acre better than the worst case. Should USDA reconcile feed and residual in the WASDE report and find exports are optimistic in future months, the market price will make moving 4 million acres from corn to soybeans a cake walk. We only planted 90.8 million acres in 2024-25!

The point in all this? There is a lot of data for the data-driven folks to yet see and absorb without even considering the weather. As usual, price discovery will help with decision-making. The increase in a floor under prices via changes in crop insurance could once again influence planting intentions, regardless of what price discovery suggests.

December corn futures had a range from the top Feb. 12 of $4.80 to 90 cents lower by late August to a rally of 50 cents from that low as of last week, and for now haven’t been able to close consistently above the July 6 high I have mentioned repeatedly. That is a swing of $1.40, or $280, on 200-bpa corn. This seems to give risk management a whole new meaning. Something to ponder when prioritizing what is important in management.

Jerry Gulke can be reached at (707) 365-0601 or by email at Jerry@gulkegroup.com

(c) Copyright 2025 DTN, LLC. All rights reserved.