Gulke: Year-to-Date Overview

The views expressed are those of the individual author and not necessarily those of DTN, its management or employees.

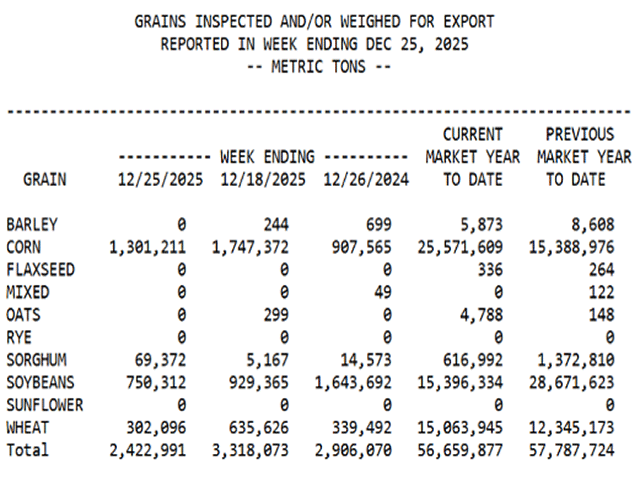

(USDA table)

As we print the last trading day of 2025, we also end the first quarter of the marketing year 2025-26. The latest export inspections report below for the first quarter of the marketing year offers a decent outlook on prospects for meeting the USDA final export estimates, especially for corn and soybeans.

Corn is on tap for a three-peat of year-over-year increases in exports with a record for the current marketing year. A month ago, inspections were nearly 9 million metric tons (mmt) ahead with this week’s report increasing that to more than 10 mmt. This keeps exports easily within USDA’s target with a possible further increase in the Jan. 12 final WASDE.

Soybeans have been in a cloud of negativism since the first big China framework meeting in early November. Subsequently, the market topped in a background of doubts China would actually meet soybean buy projections. China has indeed purchased about 80% or more of the 12 mmt promised and have in fact bought beans for 2026-27 marketing year.

Nevertheless, while loadings a month ago were 10 mmt behind last year, the current report shows that gap widening to 13 mmt, suggesting doubts that soybean exports will meet USDA projections. Adding further uncertainty is the delay in EPA rulings on the RFS decisions, perhaps until late in Q1 of 2026, when it may be too late for producers to revise planting intentions. Unlike the hot corn market, non-China purchases have not been able to sufficiently fill the export gap, and the record Brazilian crop will offer stiff competition next month and into the 2026 harvest.

The Jan. 12 WASDE has its importance from a corn yield standpoint. A majority of producers and traders expect the corn yield to be reduced, while price action and large spec positions suggest otherwise. With the feed and residual use estimate still in question, there is room to lower yield and feed demand, which leaves doubts the resulting ending stocks will be lowered. Soybeans have their problems getting a bullish report. A bullish reduction in yields is needed.

Planting intentions seem to have less to do with prices than with government intervention. Government bridge payments, crop insurance changes and lack of China framework details make corn acres the winner in my book as it stands now. From a banker’s standpoint it seems reasonable to loan enough capital to buy up corn insurance to the 95% level and let RMA pay to insure breakeven. The perception of soybean’s negative cash flow adds to the mix of difficulties of cash flow in grain/oilseed production.

I mentioned in this column 18 months ago that I felt there had been a paradigm shift in the way we will do business globally. Government influence, intervention, lack of timely decisions and the eco/political uncertainties that lie ahead all play a part — but price risk management is still valid. As price charts have shown over the past year, there have been opportunities for enhancing profit and odds are 2026 will be no different. Adding 10% to the bottom line via risk management should be a minimum goal. We have the tools to do so.

The biggest concern is the lack of acceptance of risk management as designed decades ago, nor the passion to do so. It is not hard to be in the top tier of success. The difference between the salary of a 200-baseball hitter and a 300-hitter is huge in today’s market but only requires one more hit per 10 times at bat. A $10-$20 per acre increase in bottom-line profits in today’s margin-thin economy could be huge in success or economic malaise.

A review of the price volatility of nearly all grains/oilseeds shown in this column over the past year reflects graphically the opportunities in the marketplace no matter who is our president or what party has control. I bet Elon Musk would love to have the opportunity to lock in 100% of his production with one phone call to his broker.

Money is not everything when it comes to measuring success, but it is the only way to keep score.

Jerry Gulke can be reached at (707) 365-0601 or by email at Jerry@gulkegroup.com

(c) Copyright 2026 DTN, LLC. All rights reserved.