Gulke: Deal or No Deal?

The views expressed are those of the individual author and not necessarily those of DTN, its management or employees.

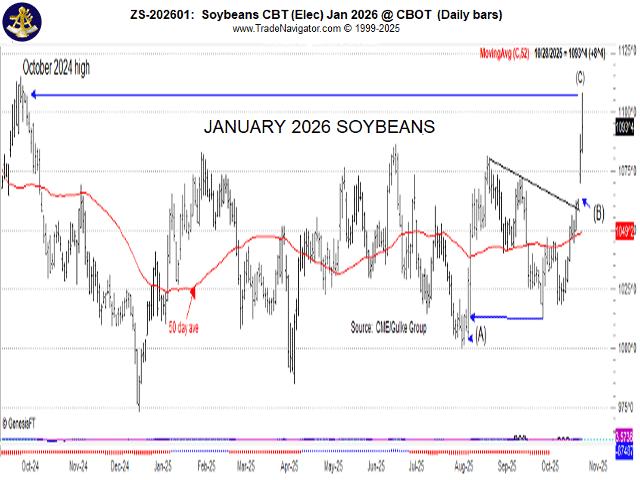

Point (B) on this chart of January soybeans trade is the high area posted by soybeans on Oct. 1, 2024. Prior to 2025, October harvest time was when highs were posted for the marketing year going forward. Until this week, only corn had exceeded the October 2025 high. Wheat certainly hasn’t, and not until this week did soybeans try. (Chart by Gulke Group)

With the federal government shut down and departments yielding little to no information, seemingly little analysis is being produced by data-driven media analysts. The craving for info that the data-starved media has shown demonstrates how fragile rational outlooks are indeed. This has made the evolving news on a China deal the only game in town. Meanwhile, global markets have been trading our commodities, albeit with bated breath. This has forced some to revert to technical action and referencing price charts to try to get some semblance of direction. Market analysis that I have heard or read recently leaves a lot to be desired.

Maybe I should give recent price discovery some clarification.

The January soybean chart accompanying this week’s column is next in line, as November futures are facing first-notice day, and no one would really want to risk trading November, as volatility could explode under a limitless trading environment.

Soybeans posted a daily and a weekly gap higher. I have referenced in past columns the importance of the July 7 gap lower, construed as negative. The gap higher this day/week leaves what astute analysts would recognize as a trading island marked by a gap lower and gap higher over the July 7 to Oct. 27 gap higher. If this is something new to you, contact me, as I have a book my daughter and I authored entitled “Technical Analysis – Fundamentally Easy” that I have used as a tutorial in analysis, which I would gladly send you.

The definition of the trading island market by a gap up (B) is tantamount to saying, “Anything you knew or thought you knew is now old news.” In other words, the paradigm shift in agriculture trade I mentioned a year ago has been emphasized. However, there is some history here and important price-discovery information. Of course, the trade will say it was President Donald Trump’s prospective deal with China that is the cause. Never mind that harvest lows were posted much earlier, and buy signals prompted me to re-own 100% of cash forward sales 40-50 cents ago.

But wait, there’s more!

Point (B) just happens to be the high area posted on Oct. 1, 2024. You will recall me pointing out the significance of corn, soybeans and wheat sustaining a close above the previous harvest highs made in October. Prior to 2025, the October harvest time posted highs for the marketing year going forward. Until this week, only corn had exceeded the October 2025 high. Wheat certainly hasn’t, and not until this week did soybeans try.

January soybeans, in their near-hyperbolic move, accelerated to that October 2024 high and have not yet closed — nor sustained a close — above it, unlike the bull move last year in corn that topped out on Feb. 20.

In recognizing this event, it is helpful to know an important psychological point. The high in October 2024 was reached without knowing that China would stop buying soybeans from the U.S., and indeed it did, until this fall, when it normally buys at least 10 million metric tons (mmt).

Rumors abound now that China will indeed buy 10 mmt to bridge the gap to January/February 2026 when Brazil’s harvest supplies China’s needs. A token amount was purchased last night; it was reported as a good-faith gesture.

So, all soybeans did were to reexamine what the price would be, all things being equal, and if China were buying U.S. soybeans. U.S. soybeans store better and are bought by the Chinese government for that purpose, whereas crushers will buy from Brazil for immediate and constant crushing needs.

A lot will be learned when details of the “framework” are announced. My concern is that the wording might be a repeat of Phase I, leaving China a way out but still producing an agreement that will be touted to be good for U.S. agriculture. Let’s hope that reality exceeds anticipation. We will know soon as we begin a new month, which has the task of continuing the past uptrend.

Jerry Gulke can be reached at (707) 365-0601 or by email at Jerry@gulkegroup.com

(c) Copyright 2025 DTN, LLC. All rights reserved.