Gulke: Heading Into February

The views expressed are those of the individual author and not necessarily those of DTN, its management or employees.

Per-acre prices of recent farmland sales. (DTN graphic)

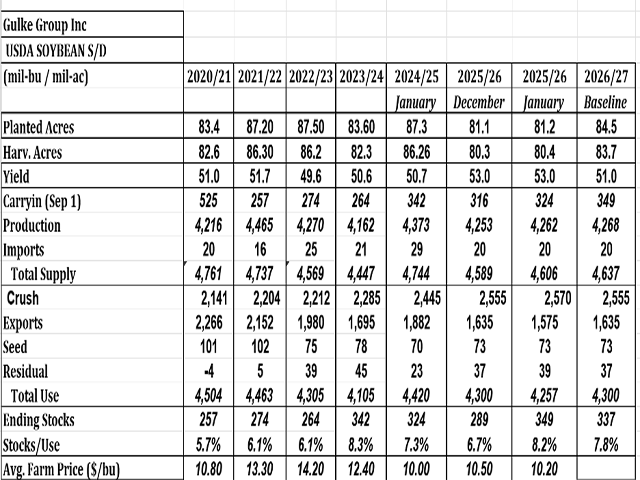

A lot will happen in February to fundamentally influence planted acres. Last week, I reviewed the corn supply and demand outlook based on preliminary USDA ideas. These budgetary estimates are just that — estimates stemming from baseline calculations by the OMB (Office of Management and Budget) using economic models based mostly on conditions from two to three months prior. The soybean baseline numbers look interesting.

The OMB is assuming a 3.3 million-acre increase in soybean acreage. Historical precedent shows that over the past six years, acre changes have exceeded that amount, with last year at the low end of the spectrum. In 2021 and 2022, acres held at 87-plus million. With the crop insurance trigger prices ahead, more acres could swing toward corn if December futures fall further.

ACRES AND YIELD RAMIFICATIONS

The need for more soybean acres is self-evident. Even with 3.3 million additional acres, ending stocks don’t increase. A 1-million-acre swing changes the carryout range to 388 million bushels (mb) on the high end to 286 million on the low end. Obviously, current prices for November 2026 do not reflect sub-300-mb carryout.

The USDA baseline does not assume a repeat 53-bushel-per-acre yield. Either there is something we don’t know about future revisions for last year, or odds don’t favor back-to-back record yields, in their mind. A bushel change either way is significant; a 1-bushel yield change is more significant to the bottom line than a million acres more or less.

The demand side of the equation reflects usage of 43 million bushels higher than last year, driven by increased exports but surprisingly showing a reduction in crush. Crush looks understated given the trend, or alternative feed stocks will compete for the crush. Allowing used cooking oil (UCO) imports may be the culprit, but this allowance does keep crushers from mothballing plans for existing plants by providing assurance that feedstock supplies won’t be a major concern. However, a hiccup in soybean production or Chinese non-compliance with the “deal” would curtail UCO availability.

Initial results of a media survey suggest it would take either a 50-cent rally in corn or a dollar rally in soybeans to change acres much. But like last year, the devil is in the details. If something doesn’t happen to facilitate those ideas soon, in 60 days, it will be the weather that will have the final say.

The bottom line: in the short to medium term, there’s significant price discovery yet to play out. It starts with the mid-February report from governmental analysts that will offer a revised opinion on acres — one that could prove immediately influential, as it was last year when prices topped three months early. Everyone knows this, including global traders.

Two caveats for thinking outside the box or being proactive: First, realize that it isn’t what we know that counts (everyone knows the above facts) — it’s what we don’t know that we don’t know that matters. Outlook is based on known facts, which are history. What lies ahead that isn’t yet apparent to the media? Our price discovery system is a “futures” business tasked with answering that question, which is why it’s called “futures.”

Second, it’s wise to watch what the government does, not what they say. So far, we haven’t seen a decision from the EPA, nor have we seen the “China Framework Deal” in detail. The good news this time under Trump 2.0 is that the China Deal reflects bushels, not merely dollars, and can be quantified. There’s no mention of corn in the deal, and any corn purchases by China would excite prices.

Timing is everything, and President Donald Trump’s Iowa speech in farm country didn’t reveal anything new. We may have to deal with the hand we’ve been dealt and let Mother Nature have the last say, as U.S. producers will plant every available acre to something.

Jerry Gulke can be reached at (707) 365-0601 or by email at Jerry@gulkegroup.com

(c) Copyright 2026 DTN, LLC. All rights reserved.