Gulke: Majoring in Minors

The views expressed are those of the individual author and not necessarily those of DTN, its management or employees.

At least two bands of heavy snow will combine to produce some extremely heavy amounts across the northern U.S. through March 15. (DTN graphic)

Over the past two days, commodity, energy and stock markets tied themselves in a knot over relatively minor developments — majoring in minors, as the saying goes. A few hours of trading triggered sweeping conclusions, including handwringing over a brief spike in diesel and gasoline prices. Yet crude oil is $40 off its highs, and prices moved so fast I never even had time to fill my tank before calls went out to tap the strategic petroleum reserve.

Notably, it appears to be the same senator who, five years ago, wanted gasoline prices pushed high enough to force consumers into electric vehicles and drive fossil fuels into extinction. Now those spots have changed? It is a reminder that the people we elect don’t always serve us well.

Last week’s column covered the ABCs of marketing — an attempt to offer a commonsense framework for thinking about market outlook. I’ll be direct: I am tired of watching commentators with no apparent understanding of price discovery hold forth in the media. After decades of working to educate people about the process, little has changed. If anything, crop insurance and guaranteed revenue programs have displaced genuine risk management thinking — to the point where even some bankers have set aside common sense in favor of government insurance schemes.

Last week’s soybean chart ended on a question: Was the price rally since Jan. 2 a meaningful signal, or merely a blip within a longer-term decline driven by Brazil’s growing competitive advantage? In other words, was the trend strong enough to carry soybean prices higher, or would it ultimately fail?

For roughly 18 months, most market participants have argued there is no economic justification for China — or anyone else — to buy U.S. soybeans. Some analysts have built entire careers on that narrative, even as soybean prices climbed to levels not seen since January 2024, when China first began snubbing U.S. beans. Those naysayers missed something important: The economics did work, just not for the reasons they assumed.

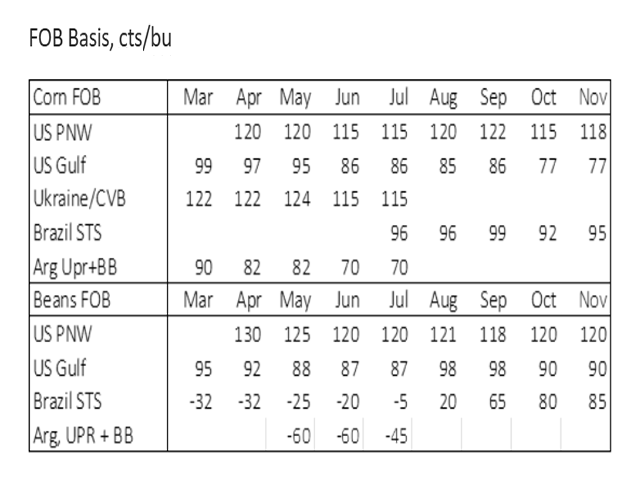

The chart accompanying this week’s column illustrates the point. It maps CNF (cost and freight) prices at major ports of departure against the buying economics for key importers. The math is straightforward and shows, at face value, where the U.S. is — and is not — competitive in soybeans, corn and wheat.

The soybean story is the most obvious. Despite widespread skepticism, U.S. soybean export pace is running only about 10 million metric tons (mmt) behind last year — which explains why President Trump is pushing China to buy an additional 8 mmt this year. If that happens, the U.S. could run out of soybeans unless USDA’s planting projections hold up. USDA is projecting an increase of more than 4 million acres, which translates to roughly 200 million additional bushels. Even so, 200 million bushels may not be enough. Do the math.

Corn’s competitive window is more time-sensitive. U.S. corn typically loses its price edge later in the summer once Brazil’s safrinha crop hits the market — but will that dynamic hold this year? December 2026 corn futures haven’t traded at current levels since June 2025, when USDA significantly raised acreage estimates. (Those estimates still fell well short of our survey’s projection of 98 million acres, a figure the market didn’t reflect until January 2026.) Something in this market knows something the public commentary does not.

Consider this: Last Sunday night, someone paid $4.98 for December corn. Naysayers will claim it was short covering, but the net position of the large spec has been narrowing from an extreme 300,000 net-short contracts back in October 2025 to a net short of 251,000 contracts in January 2026 to currently 130,000. In reality, the large spec was buying during the last four months; he didn’t just start last Sunday night. It looks to me like another episode where something happened that certain advisers had confidently declared would not happen for years.

The key question now is whether current price levels are sustainable through the rest of this week and into the March 31 Prospective Plantings report. I wrote earlier this year that by the time the market fully appreciates that there is more driving price discovery than tariffs and war, it will be too late — we’ll be in the ground planting, and it may not be enough acres.

Perhaps this column is a bit pointed today. But if it prompts you to think independently rather than follow the crowd, that’s the goal. If you feel you’ve been led astray by the prevailing narrative, reach out — we’re happy to walk through the analysis.

One final thought worth contemplating: For years, I have argued that it is past time for importing nations to hold meaningful grain reserves rather than relying entirely on the U.S., Brazil and Russia to serve as the world’s pantry for corn, soybeans and wheat. The phrase “strategic food reserves” comes to mind. If today’s geopolitical and economic turbulence isn’t sufficient justification, then nations banking on just-in-time food supply will deserve the consequences. That model may work for John Deere, but it does not work for food security.

Jerry Gulke can be reached at (707) 365-0601 or by email at Jerry@gulkegroup.com

(c) Copyright 2026 DTN, LLC. All rights reserved.