Gulke: Shock and Awe

The views expressed are those of the individual author and not necessarily those of DTN, its management or employees.

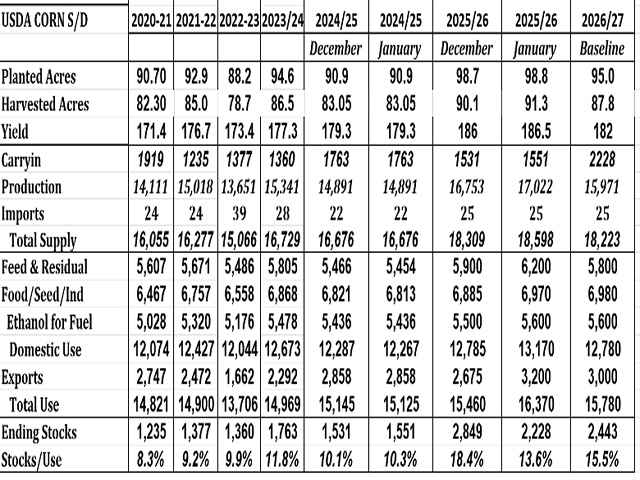

This table shows long-term supply and demand. (Chart by Gulke Group; USDA data)

The media is full of shock and awe Tuesday after Monday’s World Agricultural Supply and Demand Estimates (WASDE) report — especially in corn where corn “took back” nearly 30 cents per bushel right off the top. That likely represents mostly any profit left in old-crop corn. At 200 bushels per acre (bpa), that amounts to nearly $60 per acre or $60,000 per 1,000 acres and $600,000 on 10,000 acres. That should put to rest ideas that using futures and options is too time-consuming and/or too expensive.

Last week, I reminded readers that the worst nightmare for a bullish producer holding old crop would be if WASDE did not lower yield(s) but somehow raised carryouts for either or both corn and soybeans. I further related, again, that the data-starved media trading gurus were confused, which was leading again to cheap options protection for both bulls and bears. I suggested if your broker couldn’t think out of the box, give me a call and perhaps I could help. My phone didn’t ring once! Perhaps it is apathy or an unconcerned attitude that if things get worse, President Donald Trump will issue more checks. Regardless, it is concerning.

Some noteworthy corn comments derived from the WASDE report caught my attention.

— Although the world corn carryout increased almost 12 million metric tons (mmt) from last year, it is still the second-lowest global carryout since 2008-09.

— China is forecast to have increased corn production 6.2 mmt over the last year and almost 12 mmt higher than two years ago.

— Next year’s U.S. beginning stocks will be the highest since 2017-18.

— U.S. Dec. 1 corn stocks of 13.3 billion bushels (bb) is a new record. Of that amount, 8.7 bb are stored on farms, up 14% from last year.

— Harvested acres were increased by more than a million, citing less silage production. USDA commented that while planted acres are determined by FSA certified data, the harvested acres are determined by farmer surveys.

— USDA stated at the time of the latest farmer survey, 415,000 acres of corn and 240,000 acres of soybeans were left to be harvested.

— USDA increased the Marketing Year Average price for corn for the month of December from $4 to $4.10, which negatively affects the PLC/ARC payment.

— Feed and residual use, viewed as optimistic, actually increased.

— Exports were unchanged.

— Bottom line, even with excellent demand, carryover stocks exceed 2.2 bb.

— Using USDA baseline acres of 95 million, 3.8 million fewer than last year and a yield of 182 bpa increases ending stocks to 2.4 bb — more if we use 186 bpa as a new trendline.

— Even assuming a 3.8-million-acre increase in soybean acres, carryout for 2026-27 will stay under 340 mb if yield is 51 bpa, not 53 bpa.

— Our worst fears that we would produce too much did, in fact, occur.

GOING FORWARD

The task now is to glean nickels and dimes to help gross income and to cut input costs. Diesel fuel quoted rack prices of $2.02 to $2.05 — cheap enough to book it or own crude oil as a pseudo hedge. Jawboning seed and herbicide suppliers is worth the effort, even for a few dollars per acre. I personally haven’t booked nitrogen for corn, thus keeping flexibility. The collapse in corn means my soybean acres will likely increase, with beans on beans very likely. I’ll add more profit enhancements via selling out-of-the-money call options for the premium; selling someone the right to own my new-crop and soybeans at higher prices as long as the new-crop outlook doesn’t change.

I have no old crop, as storing commercially was a negative, chasing good money after bad. But if old crop on-farm is a concern, selling call options for the premium is still a possibility. You can sell $4.60 call options, capturing the premium of 12 cents. While not large, it is about half the loss in price on Monday. Given the new fundamentals, you might want to sell two and regain 24 cents now that you know today what you did not know yesterday. But doing so has risk that has to be managed. If in doubt, give me a call, and we’ll walk through it.

Perhaps the biggest hurdle now is if you are still tied to the hip of your banker — he now has more control over your destiny and freedom to farm than last Friday. That is not good! Constraints will likely be put upon some producers to dictate what and how much to plant. As long as one can buy up insurance sufficient to make lending institutions come out with low risk, money will be no object.

The good news is we are more competitive in the global market by 25 cents in corn. Also, as I have mentioned before, the marketplace will often put pressure on the government to do the right thing. The action in soy oil, canola and even palm oil may be hinting that EPA, after delaying a decision long enough, sees a loss in soybean prices of over $1.40 and negating benefits of the China Framework (which, by the way, is still lacking details and is a concern for me), will finally make a decision to help the soybean cause. That would help take acres away from corn. We’ve done it before, as the long-term supply and demand table accompanying this column shows, especially when we took market signals and not political signals!

Jerry Gulke can be reached at (707) 365-0601 or by email at Jerry@gulkegroup.com

(c) Copyright 2026 DTN, LLC. All rights reserved.