Gulke: Volatility and Opportunity

The views expressed are those of the individual author and not necessarily those of DTN, its management or employees.

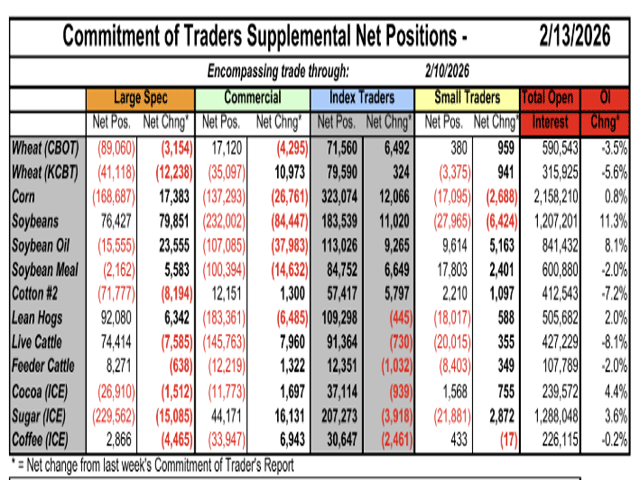

This table shows the large spec positions. (Table by Gulke Group)

Just one year ago at this time, grains and oilseeds posted highs for 2025, fell to make early harvest lows in August 2025, then rallied post-harvest to our current levels today. Using the lead contract(s) as a reference, the variation in gross income is alarming.

| Feb 2025 | Aug 2025 | Down | Today | Rally | Volatility | |

| CORN | $4.91 | $3.68 | $1.23 | $4.26 | $0.63 | $1.86 |

| SOYBEANS | $10.60 | $9.60 | $2.00 | $11.17 | $1.17 | $3.57 |

| WHEAT | $5.89 | $5.00 | $0.89 | $5.37 | $0.37 | $1.26 |

As this table shows, doing the math based on 200-bushel-per-acre (bpa) corn, 60-bpa soybeans, and 100-bpa Chicago SRW from high to low and back to today’s highs, the volatility in gross income was $1.86/bu corn ($372/ac), $3.57 soybeans ($214/ac) and $1.26 Chicago SRW ($126/ac).

Regardless of who we want to blame for the cost of production, tariffs or lack of high prices, it brings to light the opportunities in the price volatility in one year. We’d probably all want to see high prices and just stay there. But that is not reality, nor is it how the markets work. Free markets aren’t fair markets.

The above calculations are extreme but do point out that if we can capture a reasonable percentage of the opportunities that price fluctuations (volatility) offer, we can improve our bottom-line results. Our goal in 2026 should be just that.

Using a goal of trying to capture 25% of a yearly move in corn, for example, would mean roughly $90 per acre, or about 45 cents per bushel. Corn dropped $1.23 last year in about six months. That is about $60/ac. That has to be a goal this year as, according to some land grant universities, there isn’t $60 per acre of profit this year.

The same goes for soybeans, with a drop of $2. Capturing 50 cents of that is $30 per acre, again, probably more than profit expectations were a couple of months ago.

All this doesn’t take into account those who plan to store on-farm 100% of an average crop if possible. Hedging half the crop during the year and storing into spring/summer allows gains on the post-harvest rally. The case above shows corn rallying just 63 cents thus far, or about $120 per acre on a 200-bpa crop, and you still have it. Soybeans have gained about $70 per acre, most of that since Jan. 1, a time when global analysts said farmers were going to rush to sell after Jan. 1 for tax reasons. If it happened, the market absorbed it and then some, which brings up an important point. It requires dedication, good information and passion to accomplish goals.

Don’t kill the messenger, but investing time and money into risk management education is not an expense — it is an investment — no matter what your banker wants to tell you. If you don’t quite like what the market is giving you today, sell someone the right to own part of your production by selling him an $11.50 call option for 45 cents. If you can’t make money at $12 per bushel, there is little the government can do to help. There is someone out there who will pay you 45 cents for the right to own your beans next fall at $11.50. What does he know about the market that we don’t? Perhaps nothing! He is just managing his risk in case China buys another 8 million metric tons (mmt) of soybeans and/or we get a drought. He doesn’t want to be caught running his business, having to pay $14 to $15. He saw that just four years ago and got an education he hasn’t forgotten.

If you don’t like the price of Chicago July new-crop wheat at $5.35, plan to store it and sell the December $6 call option for the premium of 40 cents. If $6.40 wheat doesn’t help on 40% of your production, then I’m not sure the market will accommodate. I think you get the point.

Perhaps I have made this too simplistic, but sometimes simple is the easiest, and it keeps us from majoring in minors or overanalyzing. A simple way to help stabilize one’s thinking is to know when to hold ’em and know when to fold ’em. An example is the large spec positions shown in the table accompanying this column.

The speculator who owns a position, short or long, looking to make a profit, swings both ways. Keep in mind all the rhetoric in the media about doubting that China will honor any commitment. That person or analyst was wrong the last six weeks and is now like a deer in the headlights. What does the spec know to want him to own beans when others were advocating taking advantage of any rally? The spec knows market psychology and the law of supply and demand, however it plays out. Let’s think out of the box a little and maybe see why the spec is trying to position himself the way he is.

In my simple analysis backed by some experience, it is in the best interest of China to invest in spending $1/bu more for soybeans from the U.S. over Brazil if it means gaining billions of dollars in tariff reduction.

I wrote years ago that it was time for the importers of the world to take on the task of owning more stocks of grains/oilseeds for strategic reserves rather than letting the U.S. hold the excess stocks. The traditional pipeline to accommodate usage from old to new crop has gotten larger and more strategically evident. Stocks once perceived as burdensome have become less so. That reality may be finally coming to roost — something you don’t read about anywhere else. There, we thought out of the box a little!

Postscript: Going into what could be important reports Thursday and Friday from Ag Outlook Forum, protection via the March put or calls, good for the next two days at from a penny for corn and 4 cents for soybeans seems cheap. If the report can’t move corn 5 cents and beans 10 cents one way or another, so be it. To spend $100-$200 to protect 5,000 bushels of production is what risk management is all about. Which begs the point that maybe buying both puts and calls are a good lottery ticket?

It will be soon time for our annual Chicago Spring Outlook Conference scheduled for March 31 through April 1 (acreage report time). Click info@gulkegroup.com for more information if interested.

Jerry Gulke can be reached at (707) 365-0601 or by email at Jerry@gulkegroup.com

(c) Copyright 2026 DTN, LLC. All rights reserved.