Gulke: WASDE Surprises?

The views expressed are those of the individual author and not necessarily those of DTN, its management or employees.

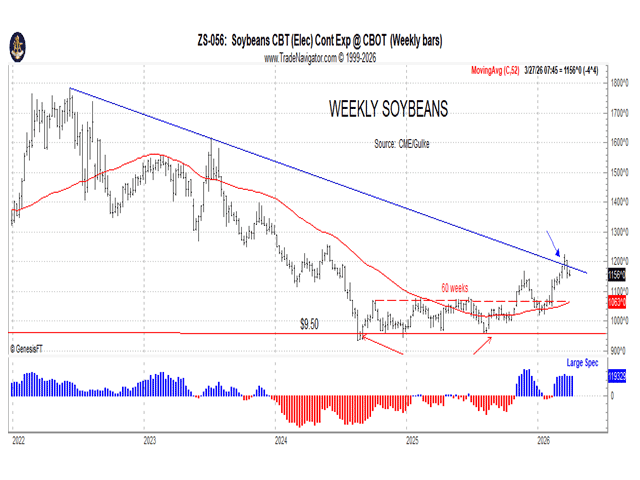

The two red arrows on this chart show the Aug. 30 dates of 2024 and 2025 and reflect very well what happened after. (Chart by Gulke Group)

With all the speculation about not only the prospective acreage and stocks reports but also the impact that the increases in fertilizer cost will have, there should be a surprise somewhere. Add to that the meeting with farmers at the White House lawn on Friday that is speculated to have good news regarding biofuels, and the plot thickens. It was suggested in this column months ago that the first quarter of 2026 would prove to be supportive to agricultural prices; that seems to have been borne out despite the volatility.

Since Jan. 2, 2026, soybeans are still up $1 per bushel (bu), wheat 70 cents per bu and corn, since the mid-January bottom, up 37-40 cents. Extrapolating on a per-acre basis, it represents a decent improvement in gross per acre to help offset the delta increase in yet-unpurchased fertilizers.

Considering the paradigm shift in ag that started 18 months ago, often mentioned in this column, the increase in prices is even more revealing. Since Aug. 30, 2024, soybeans are $2.30/bu higher, corn $1.10, and wheat $1.40, adding to the income of the on-farm stored grains that the media hype would have us believe would be ill-advised. Once again, those who are involved with production ag outsmarted most of those who are not.

Given that we are at that point where the uptrends were started, 18 months is a time period where such bullish markets run their course, as the price discovery has nearly discounted the best fundamental news to come. That means that barring a weather-induced market to help prices move from lower left to upper right on the charts (uptrend), we’d better not experience disappointment during the last three trading days of March. The 31st will likely be the market maker, unless the Friday government hype is a bust.

Based on my past remarks on soybeans, this market failed to exceed and stay above the very long downtrend (see chart accompanying this column). The two red arrows show the Aug. 30 dates of 2024 and 2025 and reflect very well what happened after. Having been turned back by the 70-cent loss last week on Monday, all that has happened for soybeans is to make a feeble attempt to rally and form what appears to be a bearish development on the daily charts (not shown).

Obviously, the results of the next few days will tell whether old-crop soybeans are experiencing a pause that refreshes or are positioning for another leg lower. Either way, protection for either event is necessary. If your broker hasn’t given any advice, we may be able to help if you are caught with beans in the bin.

July corn exceeded its November, December and January highs to recover nicely, but again, that 18-month struggle is flashing negative signals to be aware, meaning a strategy to handle a surprise is necessary. With expectations of a drop in acreage, the media bias has been for a significant cut in acres planted. The large feed and residual still in the demand side could temper bullish acres.

In both commodities, the new-crop contracts have held up better, with levels of near $5 for December corn and $12 for November beans being teased — something unexpected 18 months ago. Both of those contracts seem to be getting tired, as well, and in need of an infusion of fresh bullish news; perhaps President Trump holds those cards?

Wheat was the dog of the three for months, staying in the dumpers until Jan. 2, 2026, where it made the low to start Q1 and reached a level not seen since June 20, 2025, where it also started flashing concerns.

A lot of discussion about the volatility in grains/oilseeds has been blamed on the Iran war and on the price of agriculture energy. It is interesting that the energy market also saw lows made the first week of January, where on-farm rack prices reached $2.05 on Jan. 8. Also, the prices of soybeans, wheat and soy oil are about the same as they were on March 1 before the war, and corn is unchanged from about 10 days ago. So, there was not a lot of market gain for ag commodities during the war. Food for thought as we prepare for the next days of fundamental data to be released. Perhaps the technical picture is worth noting again — just saying!

Jerry Gulke can be reached at (707) 365-0601 or by email at Jerry@gulkegroup.com

(c) Copyright 2026 DTN, LLC. All rights reserved.