Gulke: Patience While Events Evolve

The views expressed are those of the individual author and not necessarily those of DTN, its management or employees.

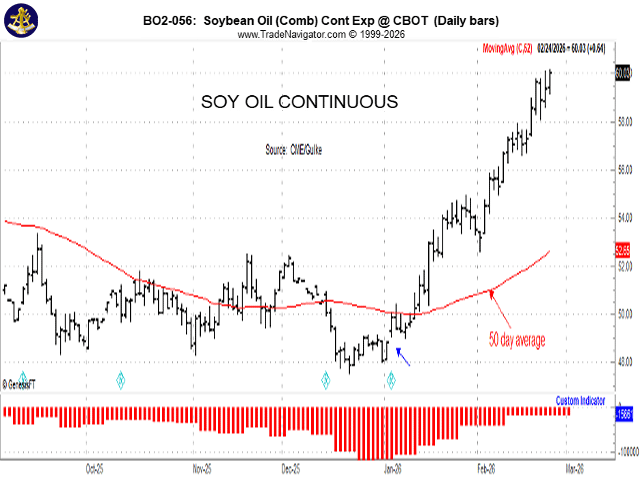

This chart depicts what the market thought about biofuels’ prospects, starting at the buy signal on Jan. 5 with the gap higher and now at highs not seen since October 2023. The red bars show the large spec is still slightly short, but the odds are, will be long soon. (Chart by Jerry Gulke)

I covered quite a few topics last week: the evolving large spec positions moving less negative to outright long; the rationale for China paying a dollar more for U.S. soybeans over Brazilian beans (that 8 million metric tons extra); the necessity for larger pipeline supplies to get us from ending one crop year to obtaining new-crop supplies; and the large spec position improvement, most noticeably affecting wheat. What wasn’t discussed was the USDA Ag Outlook Forum and the U.S. Supreme Court decision on tariffs. A review is in order.

The U.S. Supreme Court upset the apple cart at first release last Friday, but that didn’t last long. All it did was create a wider trading range for commodities, but things calmed down by the close. In fact, the three principal commodities traded at or above Friday’s close at press time; so did canola and soy oil — both biofuel feedstocks. The bottom line is that there is more evidence the structural change to agriculture looks more important than the court ruling. This has got to have the negative naysayers bewildered.

China’s decision to buy or not to buy additional soybeans before the proposed meeting with the U.S. in late March or early April is yet to be determined. Last week’s column proposed that doing so was an investment, not an expense. If they decide to increase purchases before Aug. 30 it will increase concerns about adequate pipeline supply.

The large spec trend continued. In columns past, I suggested the large spec would indeed reduce net short in favor of neutralizing positions, if not outright going net long. Last Friday’s report showed net purchases of corn up 12,950 but still net short; net sales were up 11,340, also net short but nearly 50% less short than Jan. 2. Wheat has been net short for five years. Soybeans were up 38,813 and are now net-long 115,240 contracts. The large spec was long 163,000 soybeans in November when China announced a huge buy of about 800,000 million metric tons (mmt) of soybeans. Coincidentally, the price then was about the same level as now, something naysayers said wouldn’t happen as China would never honor buying 12 mmt, and the $1.40 loss wouldn’t get traction again. It appears the large spec bought all the sales in the three majors as well as soy oil. (See that in the chart accompanying this article.)

The Ag Outlook Forum presenters I heard were excellent, and communication as to the focus was clear, concise and realistic. The chief economist allayed my concerns, and the focus on outlook was realistic and optimistic, in my mind. The biofuels presentation allowed the conclusion that the administration knows full well the potential for demand. It was not hard to be optimistic for the long term. I was especially impressed with the rep from the foreign ag service who said, “There has been a paradigm shift in how we look at marketing in the global marketplace” — something I mentioned in this column 18 months ago. The media, in general, has missed this event but likely will get on board about when it is time to sell.

Last year, prices topped around Feb. 21, surprising most traders who were anticipating highs in May or June, as is typical. But that didn’t happen. A sell signal daily and weekly was generated back then, and prices couldn’t sustain a rally back above that point for the next six months until the harvest lows came at the end of August. All these events were covered in this column. This year, everyone was pretty bearish to beans at $10.40 in early February (big Brazil crop was going to swamp all bullish hopes). Yet, we are now 100 cents higher — not 20 cents higher — 100 cents higher.

In fact, the commodities that have been in doubt, new-crop corn and soybeans, have been leading the way with soy oil exploding higher, as has canola — both feedstocks for biofuels. Perhaps looking at the soy oil price chart will help attitudes; printing the highest price since October 2023 should be interesting to contemplate.

This “surprise” rally amid a wall of worry has those selling the first rally or buying puts rethinking their biases. A look at soy oil and canola charts is a dose of reality.

This does not mean prices won’t correct if some eco-political event causes prices to lose in one day what took weeks to accomplish. Timing is everything.

Gulke Group will hold its spring market outlook conference March 31-April 1 in Schamburg, Illinois. We will discuss the price discovery process as well as supply and demand outlook and what the technical analysis tells us at our conference. If interested in exploring a more realistic outlook, contact Jamie at 707-365-0601.

Jerry Gulke can be reached at (707) 365-0601 or by email at Jerry@gulkegroup.com

(c) Copyright 2026 DTN, LLC. All rights reserved.